3Jane is Evolving

From cryptonative credit lines to fintech credit conduits

In order to truly become the internet-native financial system, DeFi must become self-sufficient across all three credit products: (a) crypto-backed (b) algo-backed (c) future-backed.

Overcollateralized lending protocols such as Aave and Morpho have clearly scaled (a). Prime brokerages and CEXs have delivered (b) in the form of margin and productized it through vehicles such as Ethena. (c) credit against repayment capacity, receivables, income, and cash flows is fundamentally absent from the cryptoeconomy, despite being one of the largest categories in traditional finance within consumer and commercial credit. U.S. unsecured consumer credit alone is roughly $1.6T outstanding (FRED St.Louis Fed).

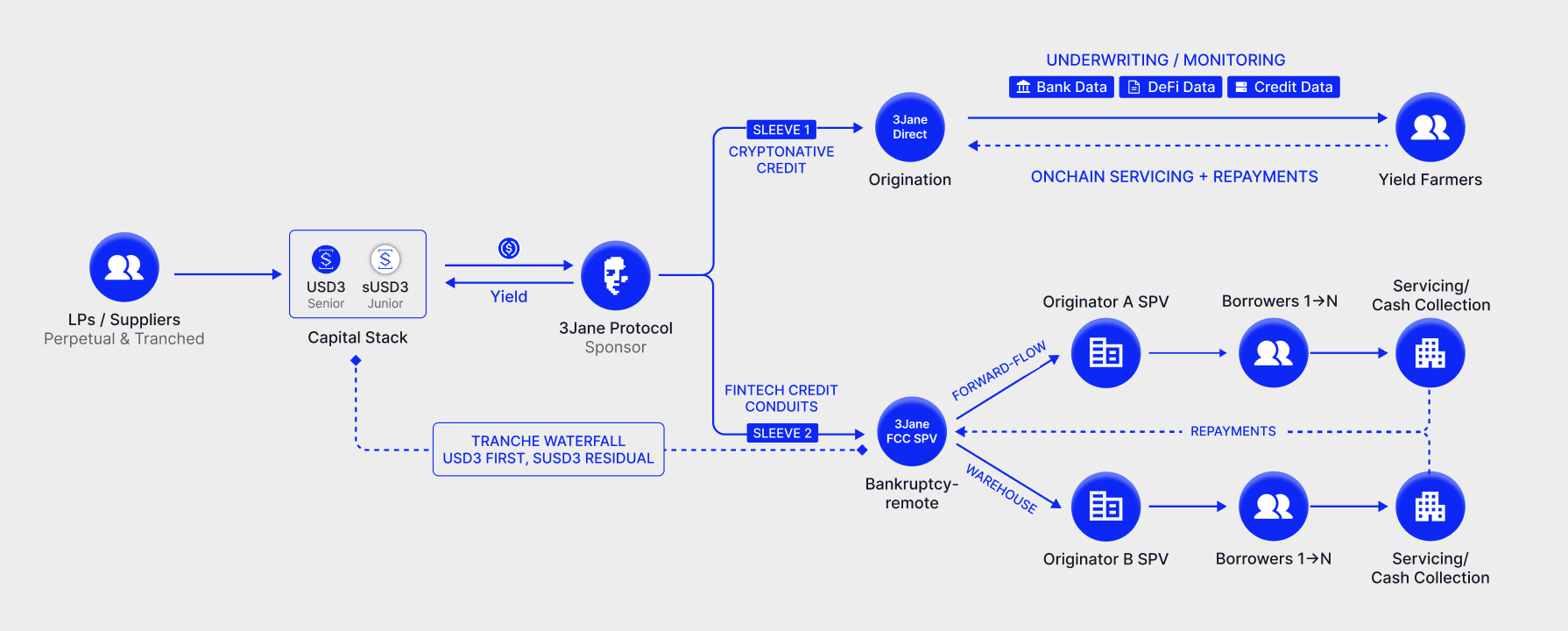

To deliver on that vision, 3Jane began as a peer-to-pool credit-based money market that issues uncollateralized USDC lines of credit to U.S.-based yield farmers. Credit is underwritten against verifiable proofs of DeFi assets, CEX assets, bank assets, future cash flows, and VantageScore 3.0 credit scores.

To accelerate our vision, 3Jane is evolving into a capital provider and structured credit infrastructure for other fintech lenders through Fintech Credit Conduits: standing, tranched funding rails in the form of warehouse loans, participations, and forward-flow agreements for short-duration SMB and consumer credit originated by other U.S. fintechs. These originators already have the distribution and proprietary underwriting models to provide financing for their end-borrower, but most cannot efficiently access forward flow or ABS markets. FCCs give them a reusable funding rail, financed through USD3/sUSD3.

As that structure scales, USD3 moves from sole Aave exposure into senior credit exposure, while sUSD3 remains junior first-loss.

3Jane V1: Cryptonative Unsecured Credit Lines

The most natural place to start was U.S.-based cryptonative yield farmers: internet-native operators with verifiable DeFi assets, cash flows, and credit data, but limited access to flexible unsecured working capital. 3Jane started by originating those credit lines directly.

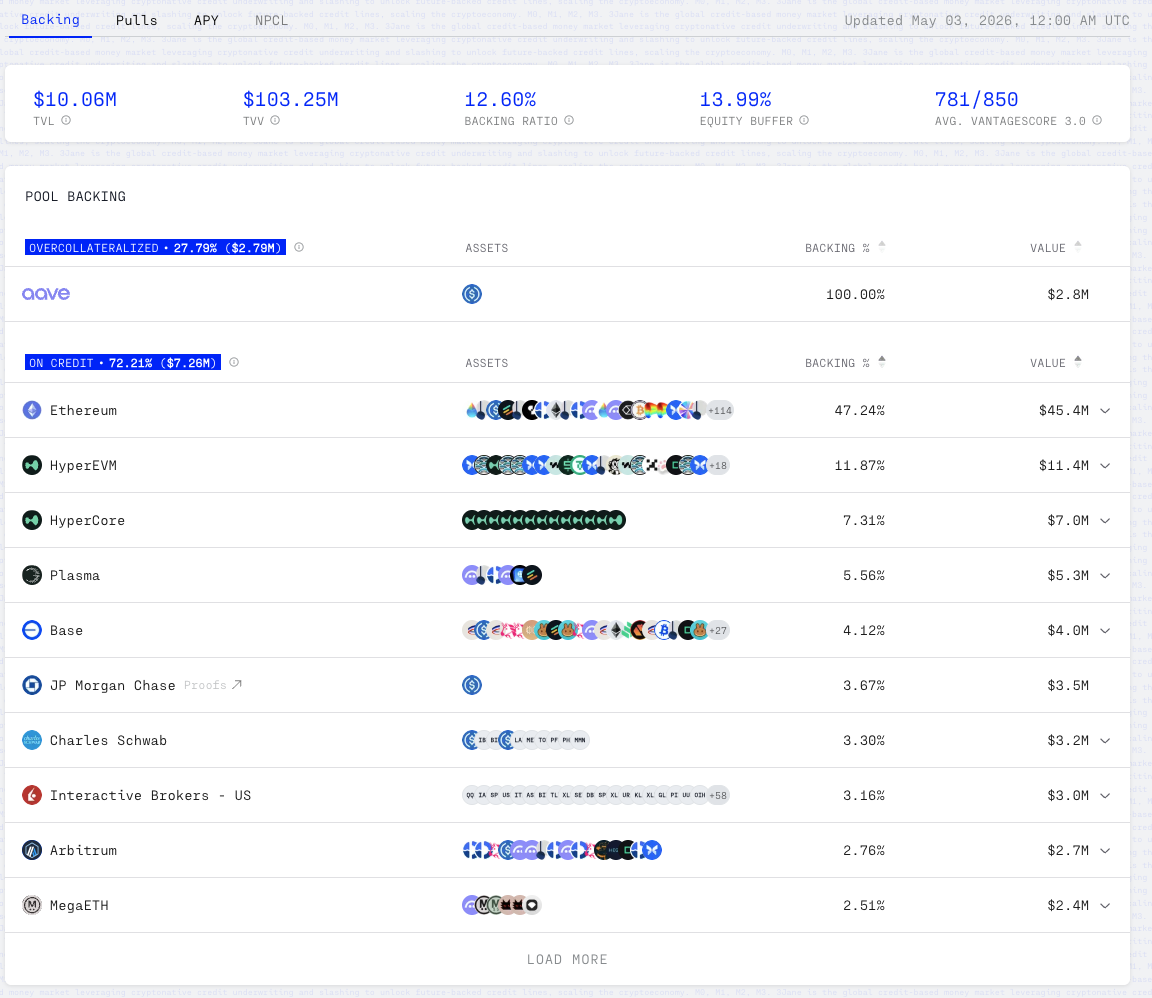

Since inception, the pool has originated ~$8M to 60 U.S.-based prime/superprime yield farmers at 376 bps over Aave borrow rates. After 7 months the pool achieved 100% in monthly payments, zero defaults, zero principal impairment to USD3 or sUSD3. The pool ran clean through 10/10, Stream, Resolv, and the worst market stretch DeFi has seen in recent memory.

The visible product was unsecured credit lines. Under the pool, the protocol had effectively collapsed the lender and capital stack into one live system: underwriting, origination, monitoring, servicing, capital recycling, senior/junior tranching, and reserve/waterfall logic. What normally sits across a lender, servicer, warehouse provider, and paying agent was running inside one protocol. We speedran the entire capital markets lifecycle of a traditional lender and had converged on the economics and structure of a revolving unrated securitization on day 1, something that takes fintech originators several years of growth to accomplish.

The Opportunity: Asset-Based Financing to Fintech Lenders

Since the 2010's, most fintech innovation has been focused on using AI and the internet to make direct origination more efficient. Companies like Affirm, Figure, and SoFi leveraged software to acquire borrowers, underwrite them better, extend loans quicker, and service their repayments dramatically more efficiently. The borrowing experience got rebuilt as software, compressing a multi-week branch process to an instant API call.

However, the capital markets side continues to operate on the same legacy rails even as the originators themselves became increasingly sophisticated.

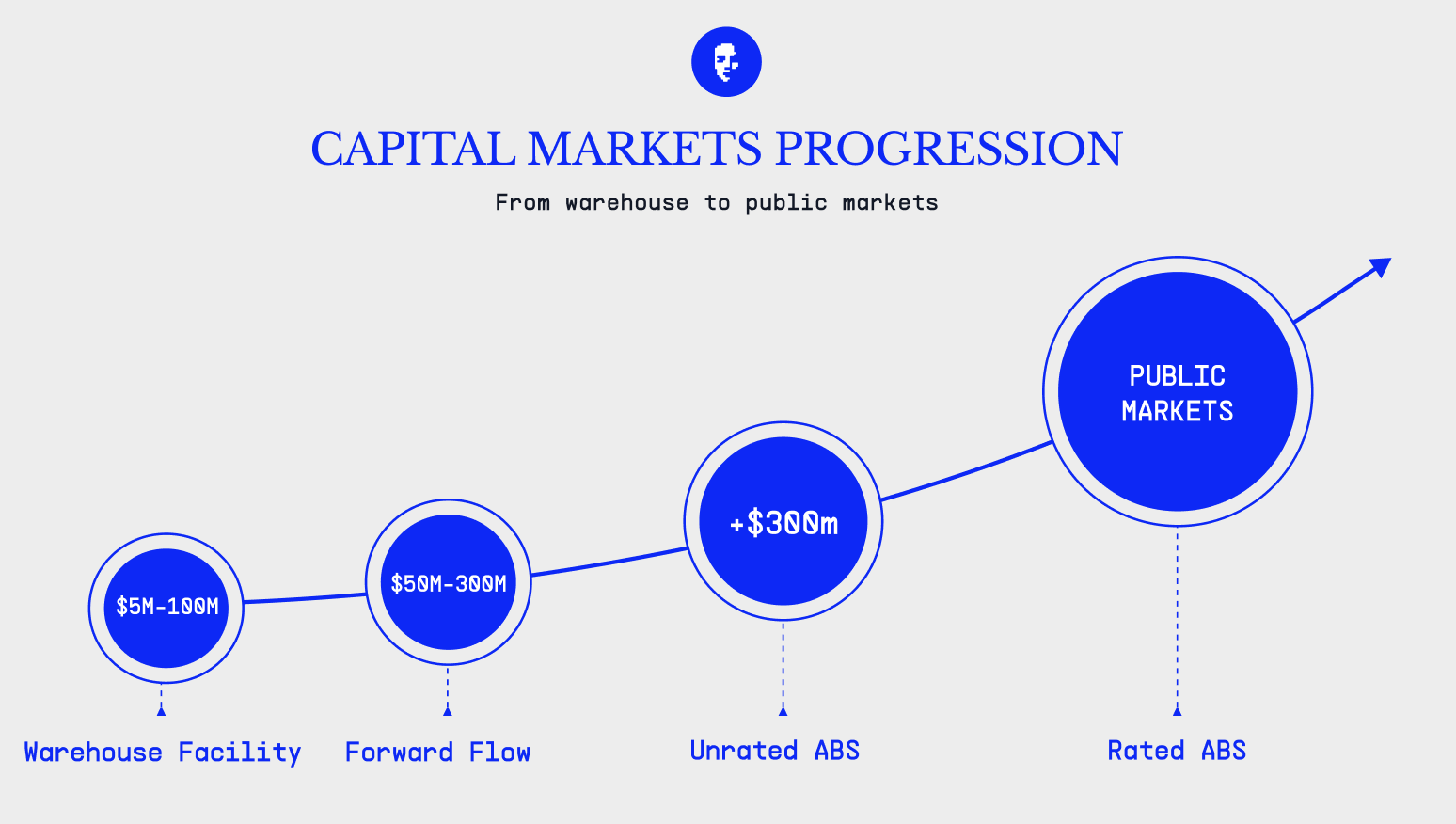

Fintech lenders scale on outside capital. They underwrite & originate loans, finance or sell them to outside investors, retain origination economics, and repeat. This is a reflexive process: as the book grows, lenders qualify for progressively cheaper funding channels, which lets them grow the book faster and move into more capital-efficient structures.

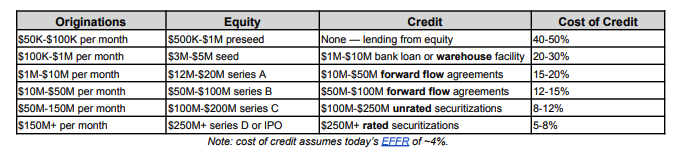

- Bank warehouse. Revolving credit line advanced against receivables, with the originator retaining a first-loss equity slice.

- Forward-flow. Whole-loan purchase agreements with asset managers and hedge funds, subject to eligibility criteria.

- Unrated ABS. Private term takeout with tranched liabilities.

- Rated ABS. Agency-rated public securitization placed with institutional buyers.

As the lender scales they converge on the originate-to-distribute (OTD) model. It moves a lender from balance-sheet-heavy growth to capital-light platform economics that produces high margins and in turn high valuation multiples.

Many originators can get to warehouse, far fewer get durable forward flow, and almost no SMB fintech / specialty lenders reach ABS programs. KBRA has rated 71 (KBRA publications) U.S. small-business ABS transactions since 2014, but repeat issuers like OnDeck and BHG account for a meaningful share of that activity. As a public proxy, fewer than ~15% (Fintech Labs) of visible SMB fintech / specialty lenders appear to have reached ABS, and repeat issuance is a much narrower endpoint.

This is a structural bottleneck where originators are too small, too bespoke, or too short-duration to be able to build the full securitization stack, rather than the assets necessarily failing. As a result there is a permanent middle market: good credit businesses capped by bilateral facilities, trapped equity, renewal risk, and capital markets infrastructure that does not compound.

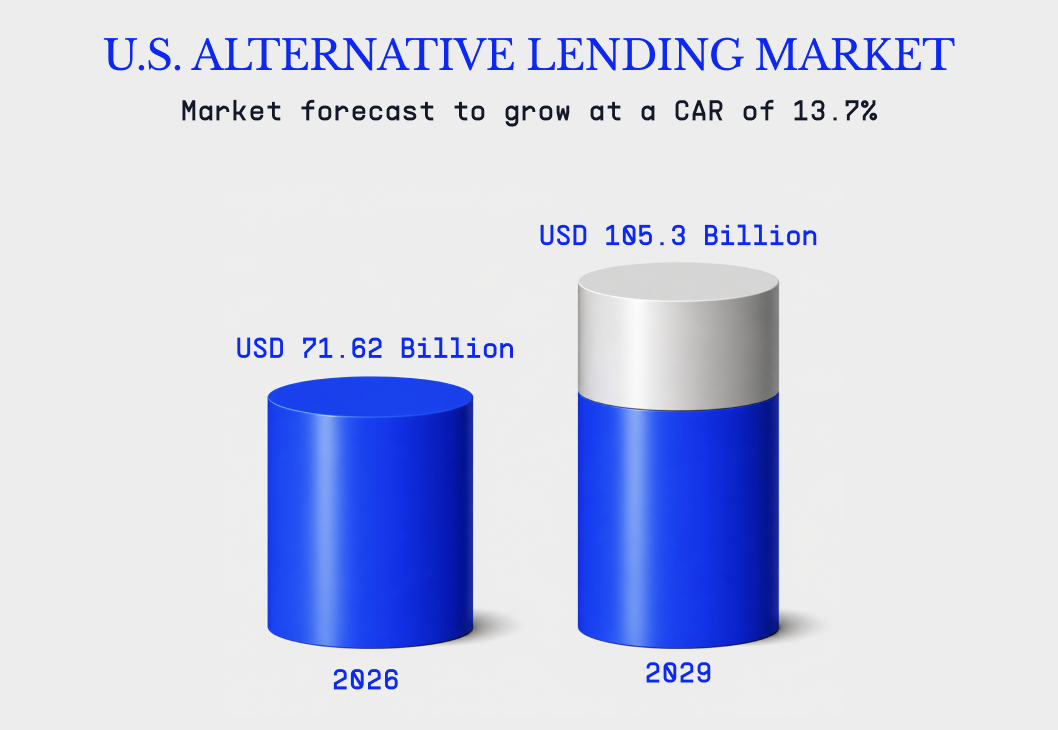

Within the $5T+ ABF category, the U.S. alternative lending market — fintech-originated consumer and SMB receivables — is projected at $71.6B of annual loan disbursements in 2026, growing to $105.3B by 2029. That market is fragmented across 100's of U.S. fintech credit originators.

The crypto thesis has always been that capital markets infrastructure can run as software, with minimal overhead as the financial complexity of the transaction arbitrarily increases. Architecturally, the distance between a simple ERC-20 transfer and a synthetic CDO on any reference is roughly a thousand lines of Solidity, Symbiotic to settle arbitrary commitments around offchain assets, and a few administrative AI agents to run the operating loop.

Figure (NASDAQ: FIGR, ~$8.13B mkt cap) identified this years ago and issued the first cryptonative S&P-rated HELOC securitization on Provenance, originating >$14B across a number of series. Earlier this year, Better (NASDAQ: BETR, ~$815M mkt cap), a mortgage lender, announced a $500M mortgage warehouse facility with Sky. This trend will only continue.

3Jane V2: Expanding into Fintech Credit Conduits (FCC's): a +$100B Opportunity

Fintechs made origination software-native, 3Jane is making structured credit programmable.

3Jane is expanding from operating its own credit book into Fintech Credit Conduits: standing, revolving funding structures via warehouse loans, participations, and forward-flows for short-duration credit originated by other fintech lenders. The conduit industrializes securitization economics, giving fintech originators private-ABS access, pricing, and scale without needing to clear $150M+/month through bankers, lawyers, and rating agencies. The architecture combines tranched USD3/sUSD3 liabilities, forward-flow purchase rails, diversified stablecoin funding, and AI-driven 24/7 structured-credit operations to compress bank warehouse → forward-flow → unrated ABS into one programmable primitive.

The key insight is that forward-flow-style purchase rails + a standing revolving tranched conduit = private ABS-like economics for fintech originators.

3Jane operates two sleeves under one USD3 (senior) / sUSD3 (junior) capital stack:

- Sleeve 1 — Direct Cryptonative Credit. 3Jane originates uncollateralized USDC credit lines directly to cryptonatives, underwritten against verifiable proofs of bank, DeFi, and credit data. 3Jane originates and holds the receivables directly.

- Sleeve 2 — Fintech Credit Conduits. 3Jane funds other fintech lenders through bankruptcy-remote SPVs as either senior secured / mezzanine warehouse facilities, participations, or forward-flow agreements. In both modes the child SPV is bankruptcy-remote, insulated from the originator and from 3Jane's sponsor entity.

3Jane bundles the parts of private securitization that originators are too small to build themselves, and that incumbent credit funds have no incentive to productize, delivering a fundamentally superior credit vehicle for both investors and originators:

- Financial-engineering advantage. Tranching, standardization, and a standing conduit let fixed securitization overhead be spread across a broader platform instead of a single lender. Originators get private-ABS-style economics earlier, without having to build their own securitization program.

- Capital-base advantage. USD3/sUSD3 creates a repeatable senior / junior liability stack backed by diversified stablecoin capital, rather than one warehouse lender or forward-flow buyer with one mandate, one balance sheet, and one renewal cycle.

- Market-rails advantage. Onchain liabilities make issuance, settlement, transfer, and distribution more flexible than bespoke private notes locked inside bilateral credit relationships. Over time, USD3/sUSD3 can plug into the rest of DeFi — collateral markets, vaults, liquidity venues, structured strategies, and settlement rails — so the liability side can compound instead of staying trapped in one buyer's book.

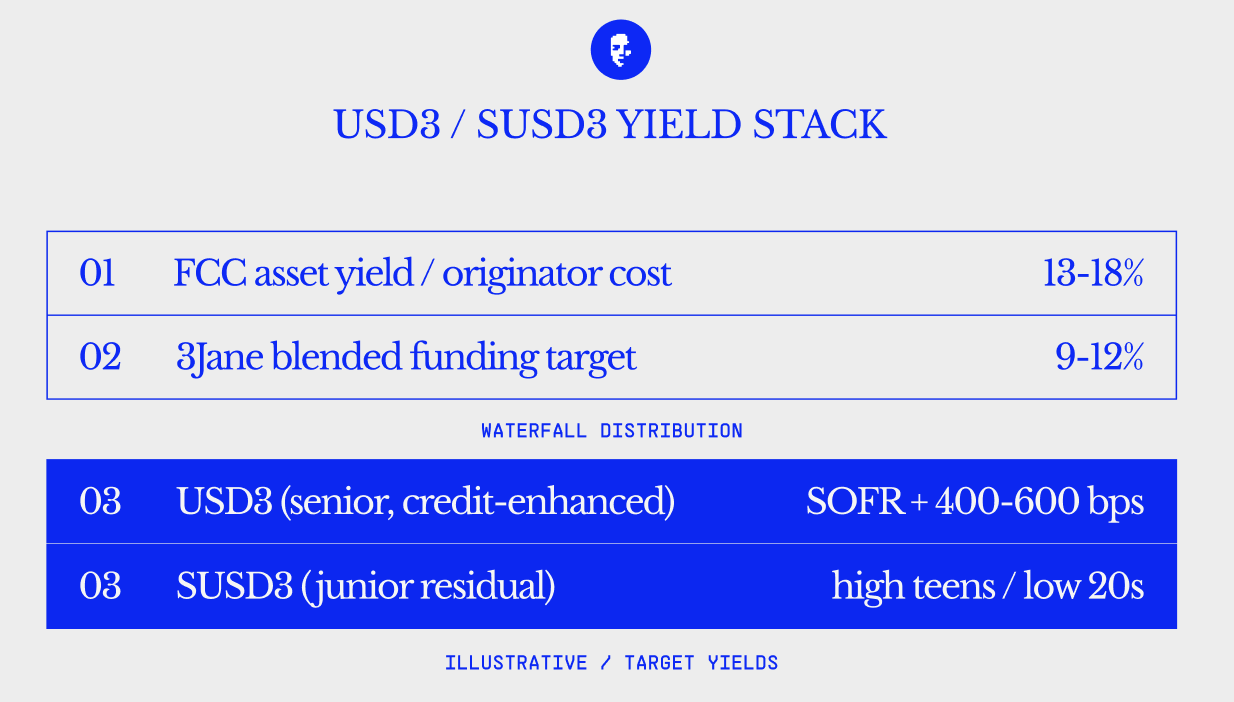

That captured spread splits across the USD3/sUSD3 stack:

- USD3 — senior. Targets SOFR + 400–600 bps APY. USD3 sits behind multiple layers of protection: pool excess spread, originator first-loss equity, overcollateralization, reserves, performance triggers, and sUSD3 subordination. In stress, shortfalls would first compress yield — including the senior coupon — before reaching USD3 principal.

- sUSD3 — junior. Targets high teens / low 20s APY after the senior coupon, fees, reserves, and pool mechanics. Losses first reduce the residual yield available to sUSD3. sUSD3 principal is impaired only after yield and applicable credit enhancement are exhausted.

Existing 3Jane unsecured credit lines stay live as a short-duration yield sleeve. In bull markets, DeFi leverage demand spikes, the sleeve grows, and these rates run well into double digits, capturing convex upside most TradFi short-duration assets can't hit. Balanced by the FCC's structurally-priced cash flows, the two sleeves diversify across duration, asset class, and counterparty, meaningfully improving the risk profile of the combined pool.

It's important to delineate that this is not corporate direct lending to software companies underwritten on EBITDA — the slice currently being questioned as AI threatens borrower terminal values. FCCs sit in a fundamentally different asset class, with LP exposure to thousands of the originator's underlying obligors rather than to the fintech itself. That diversification significantly mitigates tail risk and makes losses more modellable.

3Jane is beginning with the following type of fintech lender

- Pre-seed to Series C VC-backed, PE-backed, or bootstrapped

- $5m - $200m outstanding loan portfolio

- Less than 12 month duration assets

- Asset classes: SMB term, LOC, MCA, BNPL, RBF, factoring, and select short-duration consumer installment loans and lines of credit

What's Next

- USD3 moves risk-on next week. USD3 begins moving from bootstrap Aave / idle-stablecoin exposure into senior exposure to the 3Jane credit pool. Yield begins accruing as capital is deployed. USD3 remains senior to sUSD3 in the waterfall.

- First FCC cohort is closing. Three U.S.-based anchor fintech originators are in progress across B2B payment terms / BNPL, SMB lines of credit, and subprime consumer installment loans. Partner names, structures, and facility-level details will be disclosed at launch. The initial FCC pipeline represents $60M of target capacity, deployed in stages as facilities close.

- Capacity opens in stages. Pool capacity will expand alongside deployed FCC allocations. New capacity, allocation details, and reporting will be posted as facilities go live. Each allocation will include facility type, asset class, credit enhancement, expected senior yield, utilization, and reporting cadence.

- Farming program coming shortly. Incentives will launch alongside the senior-tranche expansion, with terms detailed in a follow-up post.

Enabling the terminal state of internet capital markets.

| Dimension | Sleeve 1 — Direct | Sleeve 2 — FCCs |

|---|---|---|

| Flow of funds | LPs mint USD3 / sUSD3 → capital is allocated to the 3Jane direct credit sleeve → 3Jane funds cryptonatives. Repayments route onchain back through the USD3/sUSD3 waterfall. | LPs mint USD3 / sUSD3 → capital is allocated to 3Jane FCC SPV / child SPVs → eligible assets are funded through warehouse or forward-flow structures. Repayments route through the originator / servicer / collection account back to the FCC SPV and then through the USD3/sUSD3 waterfall. |

| Servicing | 3Jane services directly: disbursement, accrual, repayment routing, monitoring, and tranche distribution are handled onchain / through 3Jane systems. | Primary servicing stays with the originator. Loan-tape, payment, delinquency, and eligibility data feed 3Jane monitoring. |

| Credit enhancement | 3Jane $1m insurance fund, plus sUSD3 as the junior first-loss tranche within the 3Jane capital stack. | Varies by structure. Warehouse: originator equity / first-loss piece, overcollateralization, reserves, performance triggers, and FCC SPV security interest. Forward-flow: purchase discount / excess spread, eligibility criteria, reserves, reps & warranties / repurchase mechanics where applicable. In both cases, sUSD3 provides junior protection at the 3Jane capital-stack level. |

| Eligibility | Verifiable proofs of bank, DeFi, CEX, credit, and cash-flow data. 3Jane underwriting sets limits, pricing, and credit-quality bands. | Originator-level: KYB, operating history, vintage performance, underwriting model, servicing capability, reporting quality. Asset-level: loan size, tenor, asset class, concentration caps, delinquency status, obligor / merchant quality, and consumer credit bands where relevant. Enforced at funding / purchase. |

| Loan ownership | 3Jane-originated credit lines are held directly by the relevant 3Jane lending entity / pool. | Warehouse: originator SPV holds receivables; FCC SPV holds a perfected security interest / secured lender position. Forward-flow: eligible loans are purchased by the FCC child SPV, with beneficial ownership transferring at purchase, subject to the true-sale / purchase docs. |