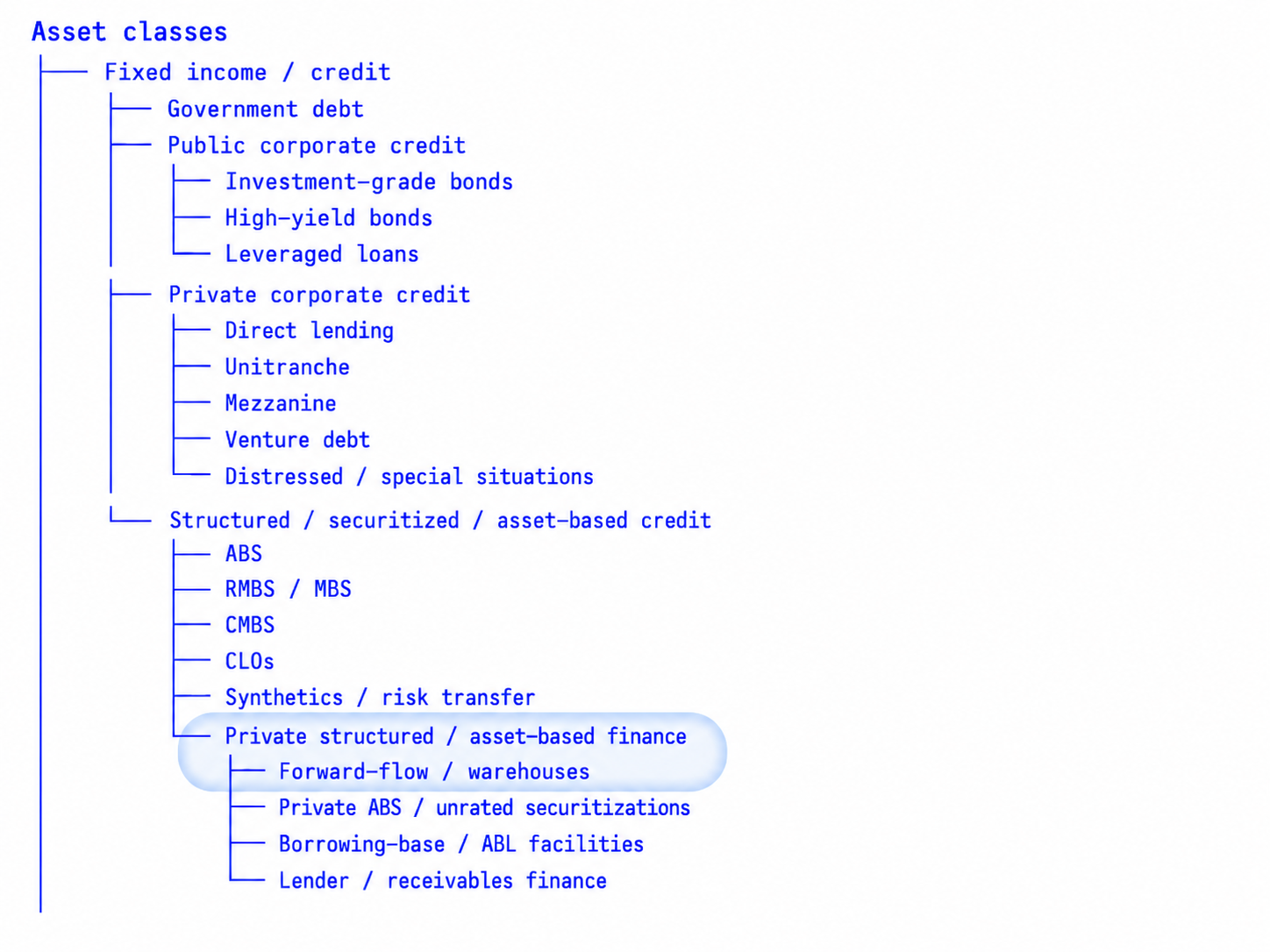

USD3 & sUSD3: ABF Risks

3Jane recently announced expansion into fintech credit conduits. Beyond operating as an existing originator for cryptonative unsecured credit lines, 3Jane is now a capital provider for other fintech lenders across a number of asset types, including SMB term / lines of credit, merchant cash advances, buy-now-pay-later, revenue-based finance, factoring, and select short-duration consumer installment loans and lines of credit.

Two facility structures are offered:

- Warehouse loans — revolving credit lines advanced against the fintech lender's own pooled portfolio of loans, segregated in an SPV.

- Forward-flow programs — whole-loan purchases of loans based on predefined eligibility criteria of acceptable loans.

Both facility structures are the predominant form of non-diluting financing for fintech lenders by banks and credit funds as a means to scale their own lending portfolio. Both structures have little to no prior history of being exported into DeFi markets with the notable exception of Figure's $YLDS backed by pooled HELOC's. As such, the general public has no experience with this type of credit product, and its risks have never been adequately mapped out.

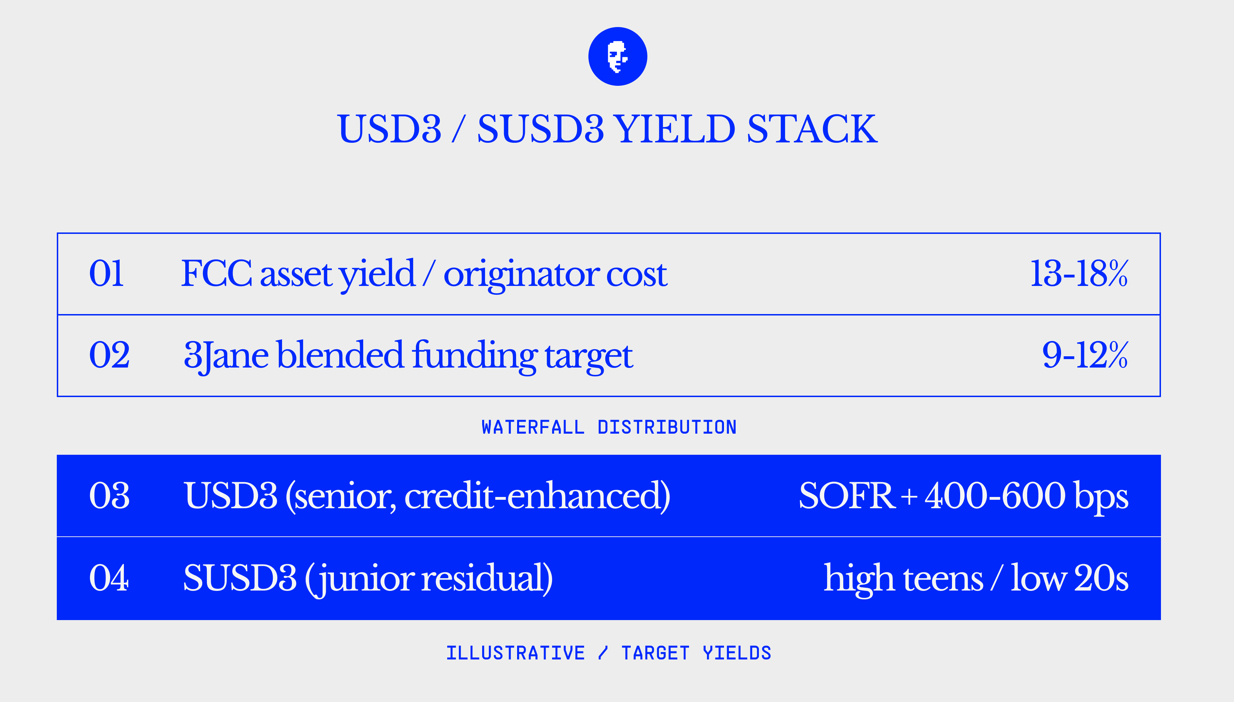

USD3 targets SOFR + 400–600 bps; sUSD3 targets high-teens / low-20s APY. The underlying receivables yield ~18% gross. The book we underwrite has run at ~1% cumulative charge-offs across vintages.

This article goes into depth on ELI5 warehouse/forward-flows, where the "yield comes from", and what the risk & loss distribution looks like.

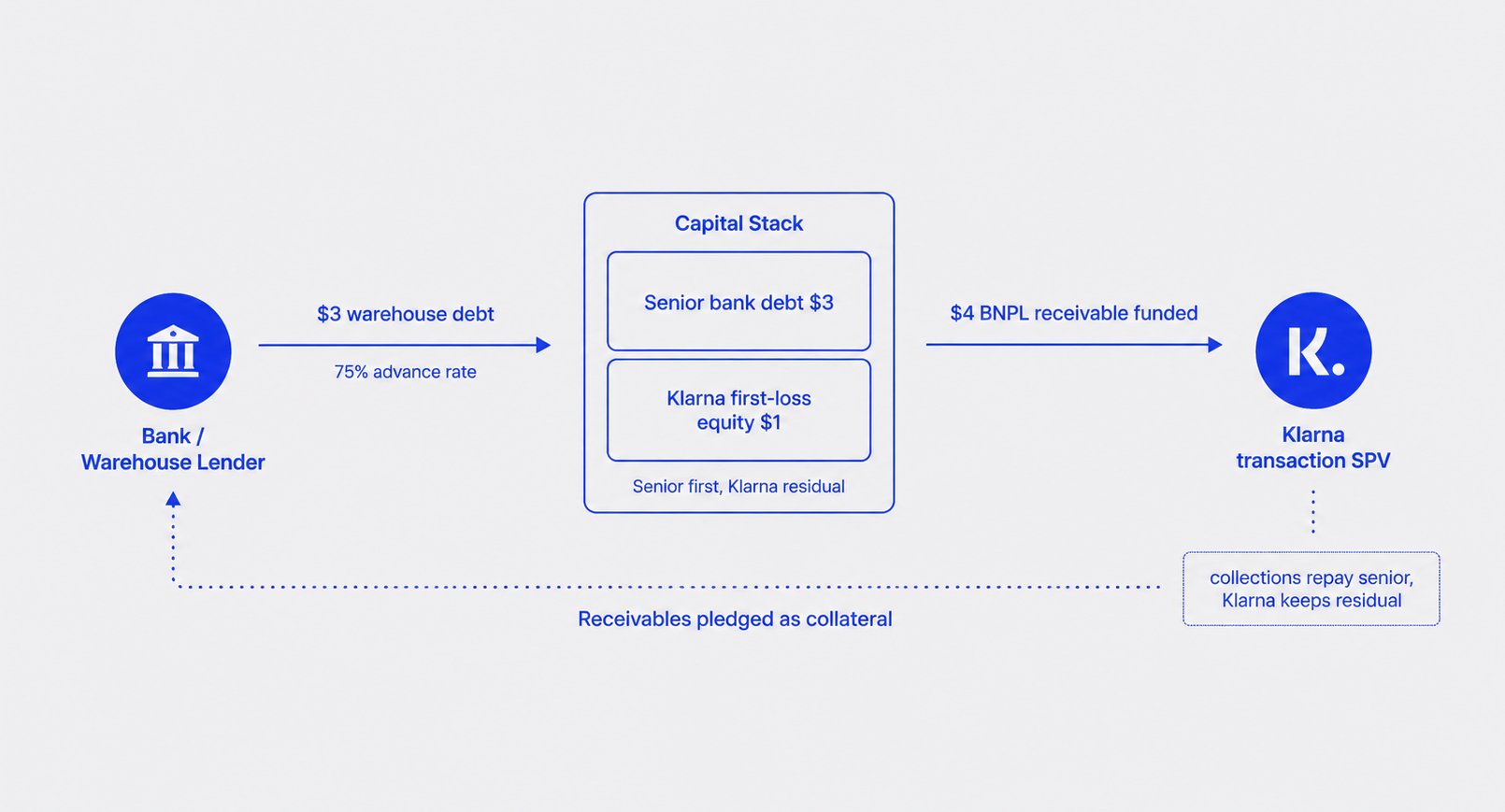

ELI5: Warehouse Loan

A warehouse loan is the lowest-lift way for a fintech lender to scale its loan book without raising more equity.

The mechanic with a Klarna-style burrito example:

- Klarna wants to fund a $4 burrito order on DoorDash. It has $1 of equity from a VC.

- A bank lends Klarna $3 against the receivables, at a 75% advance rate.

- Klarna funds the $4 order, pledges the receivable to the bank as collateral, and keeps the first-loss slice (the bottom $1).

- Consumer repays Klarna in installments. Klarna pays the bank back. The bank earns its interest. Klarna earns the economics on $4 of loans while only tying up $1 of equity.

- Same dollar of equity now funds 4x the loans. Repeat across millions of receivables.

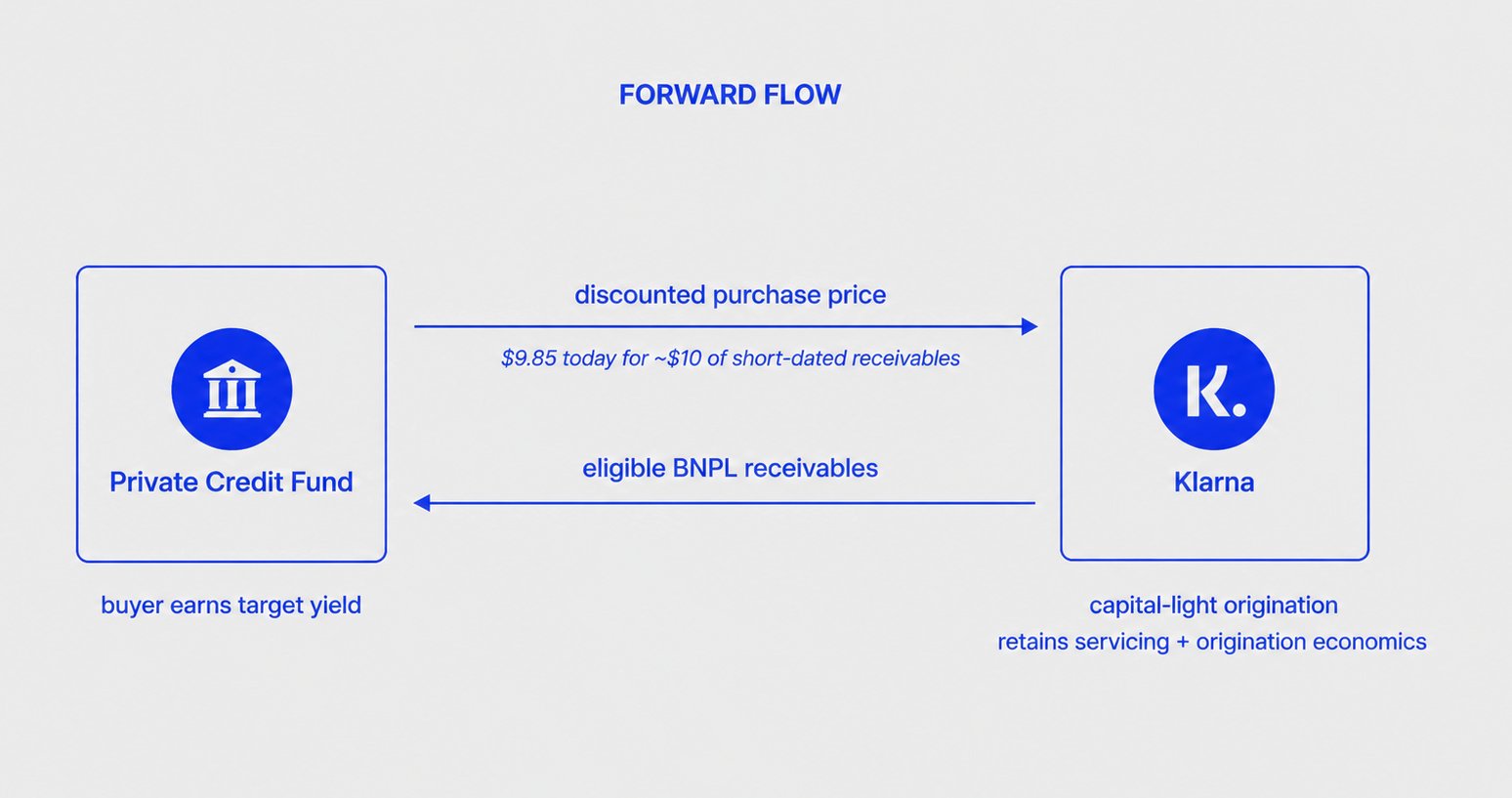

ELI5: Forward-Flows

A forward-flow is the next funding rail an originator graduates into once a warehouse can't scale fast enough.

The mechanic continuing the burrito example:

- Klarna has originated $4 of burrito loans on DoorDash, proved performance, and wants to scale to $10 of orders.

- Doing that through a warehouse would require Klarna to raise more equity to fund the next first-loss slice which is extremely dilutive.

- A credit fund offers to buy the next $10 of receivables outright for $9.85 — a 1.5% purchase discount whole-loan sale. The credit fund gets a double-digit IRR off the embedded yield in the burrito loans. Klarna gets capital that doesn't sit on its balance sheet at all.

- Klarna originates the next batch of loans, sells them on a forward calendar (e.g. weekly takedown), keeps the origination + servicing fee, recycles all of the capital.

In both the warehouse and forward-flow structures above, the cash flows reaching the senior position are contractual obligations from named end-borrowers: the 933M DoorDash customers and their equivalents in B2B BNPL and SMB lending — not the operating cash flows of the originator itself.

Where the yield comes from

Both facilities are contractual-cash-flow lending: the lender is paid from thousands of specific obligations between named parties. Cash flows are ring-fenced through SPV-level collateral mechanics: warehouse facilities are secured against eligible receivables held in an originator SPV, while forward-flow programs purchase eligible receivables into the buyer SPV on a true-sale basis.

The underlying borrowers are small businesses across a mix of product types:

- SMBs taking $50k–$250k term loans or lines of credit at 12–20% APR for inventory, payroll, and equipment

- merchants drawing revenue-based finance against future receipts at implied APRs in the 20s

- B2B BNPL: software vendors and suppliers extending 30–180 day payment terms to their business customers at 10–20% on the receivable

This APR is annualised, but these loans are short, typically 30–180 days. A B2B BNPL borrower extending a $50,000 invoice by 60 days at 18% APR pays about $1,500 in fees: roughly 3% of the loan, total. That's the entire economic cost. For a small business earning 25–40% gross margins, paying 3% to keep $50,000 working in inventory or payroll for two extra months is trivial against the margin captured on that working capital. The borrower's real alternative isn't a bank loan at 8% since banks largely abandoned small-ticket, short-duration SMB lending after 2008 because the unit economics don't work. Their real alternative is a credit card at 24%+, a personal guarantee from the founder, or slowing the business down to pay cash. While ~18% APR partly reflects credit selection, the bulk is a structural premium for speed and access: it is the cheapest source of capital actually available to them.

How it flows to USD3 / sUSD3. From the ~18% gross APR on the underlying receivables:

- The originator retains 300–400 bps for sourcing and servicing the receivables;

- Expected losses absorb another 200–400 bps depending on segment mix;

- The residual, about ~10–12% net, flows into the facility.

Yield comes from the difference between what SMB/consumer borrowers pay (~18% gross APR) and what it costs to fund them through structured liabilities. That spread, net of expected losses, servicing fees, and origination economics retained by the originator, is what flows through to USD3/sUSD3. Spread is primarily driven by complexity premium, rather than credit premium. The underlying borrowers are diversified across thousands of small obligors rather than concentrated against one enterprise.

That captured spread splits across the USD3/sUSD3 stack:

- USD3 — senior. Targets SOFR + 400–600 bps APY. USD3 sits behind multiple layers of protection: pool excess spread, originator first-loss equity, overcollateralization, reserves, performance triggers, and sUSD3 subordination. In stress, shortfalls would first compress yield — including the senior coupon — before reaching USD3 principal.

- sUSD3 — junior. Targets high teens / low 20s APY after the senior coupon, fees, reserves, and pool mechanics. Losses first reduce the residual yield available to sUSD3. sUSD3 principal is impaired only after yield and applicable credit enhancement are exhausted.

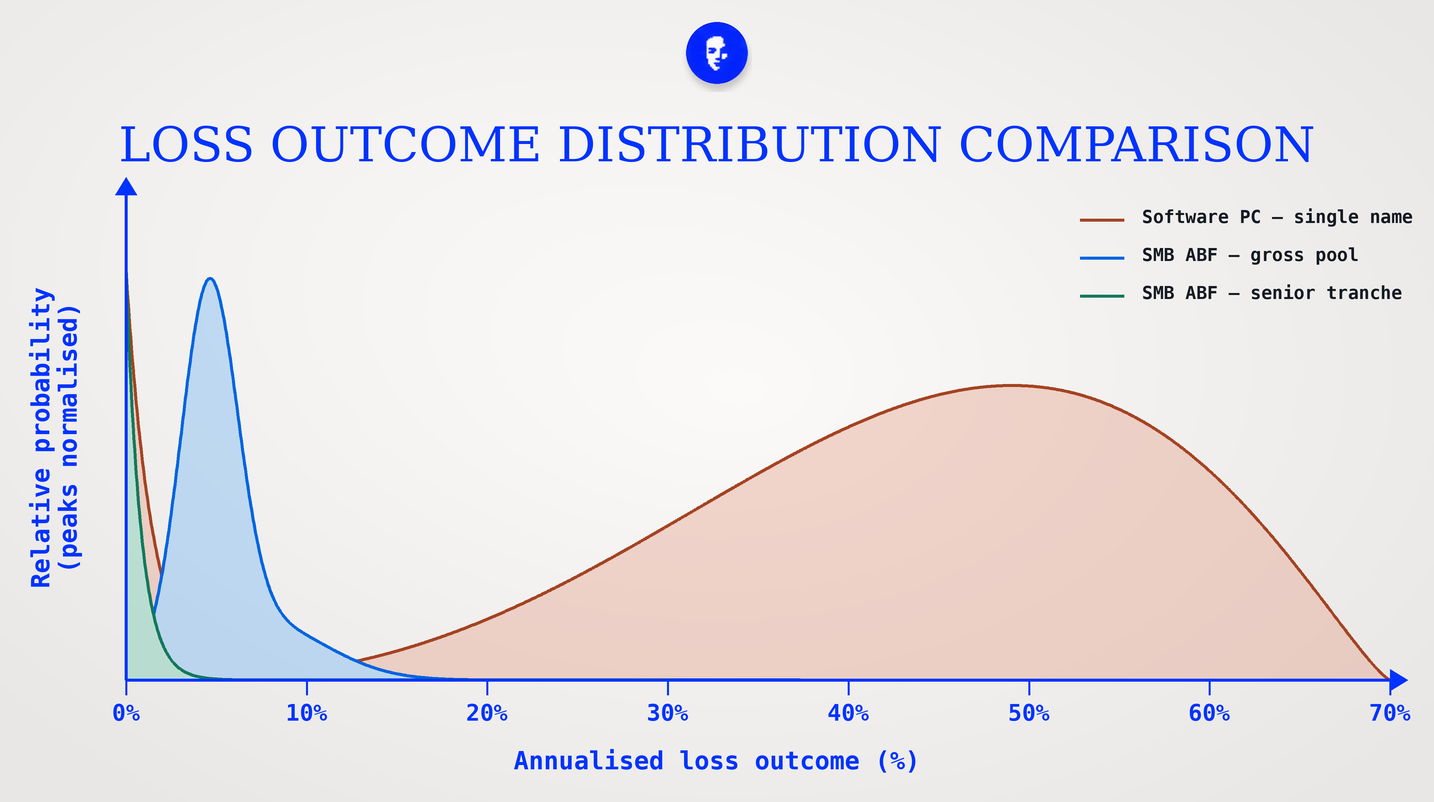

Loss Distribution

- Single-name corporate credit is bimodal: most loans pay at par, but defaults jump to restructuring-level loss severity.

- A granular SMB ABF gross pool of roughly 3,000 obligors is tight around expected loss, because each obligor can fail independently.

- The senior tranche is concentrated near zero.

- Expected loss is similar on the first two curves. The shape, and therefore the risk we are paid for, is completely different.

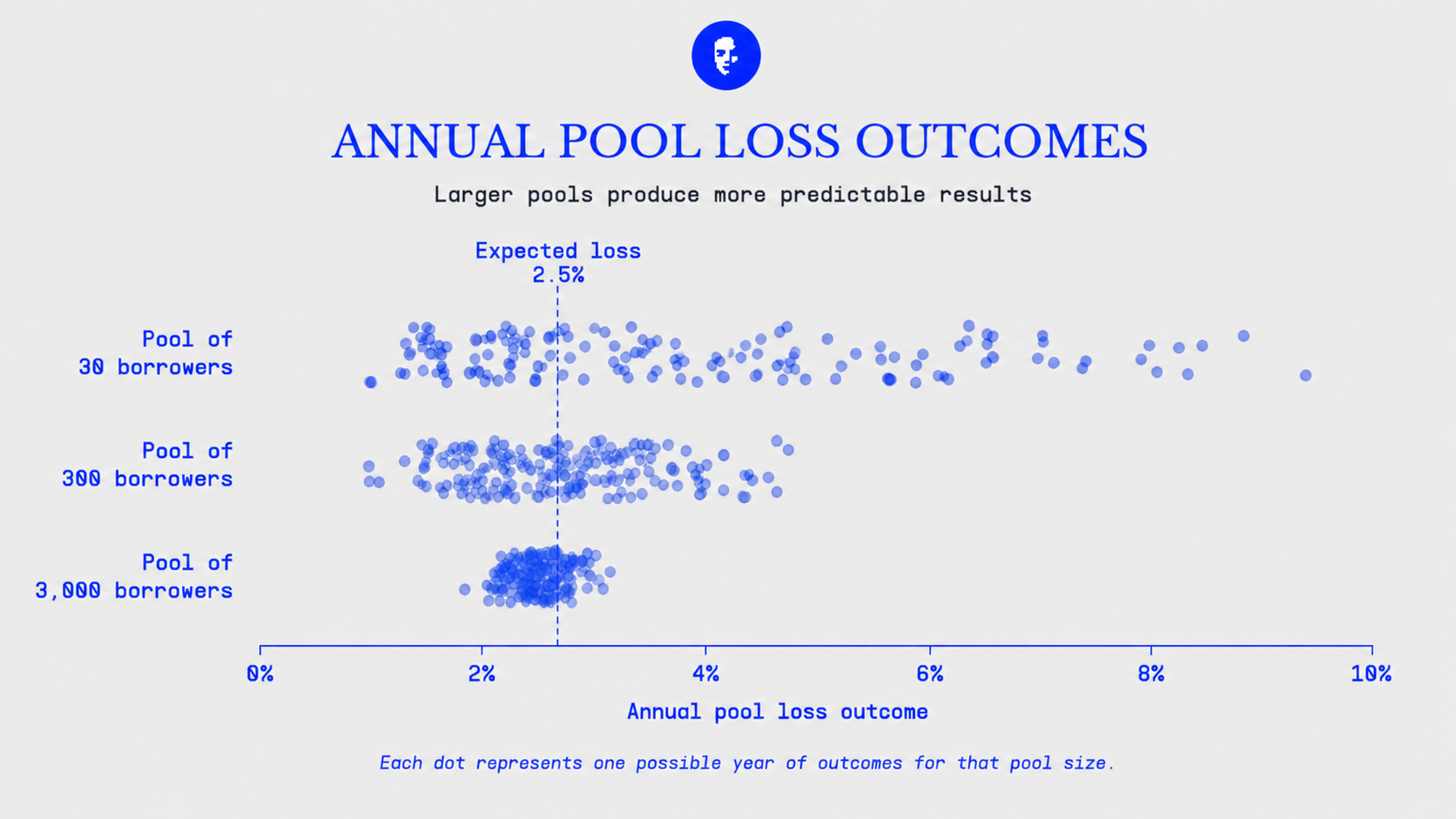

Same expected loss, very different distributions. With 30 obligors, unexpected loss is wide and fat-tailed. With 3,000 obligors, the distribution collapses to a tight spike around expected loss and standard deviation falls by roughly two orders of magnitude.

At 5% annual default probability and 50% LGD, expected pool loss is 2.5%. But the standard deviation of pool loss falls from roughly 2 percentage points at N=30 to roughly 0.2 percentage points at N=3,000. Correlation still matters, but idiosyncratic blow-up risk collapses first. Diversification compresses idiosyncratic risk. The correlation risk is handled at the structuring level.

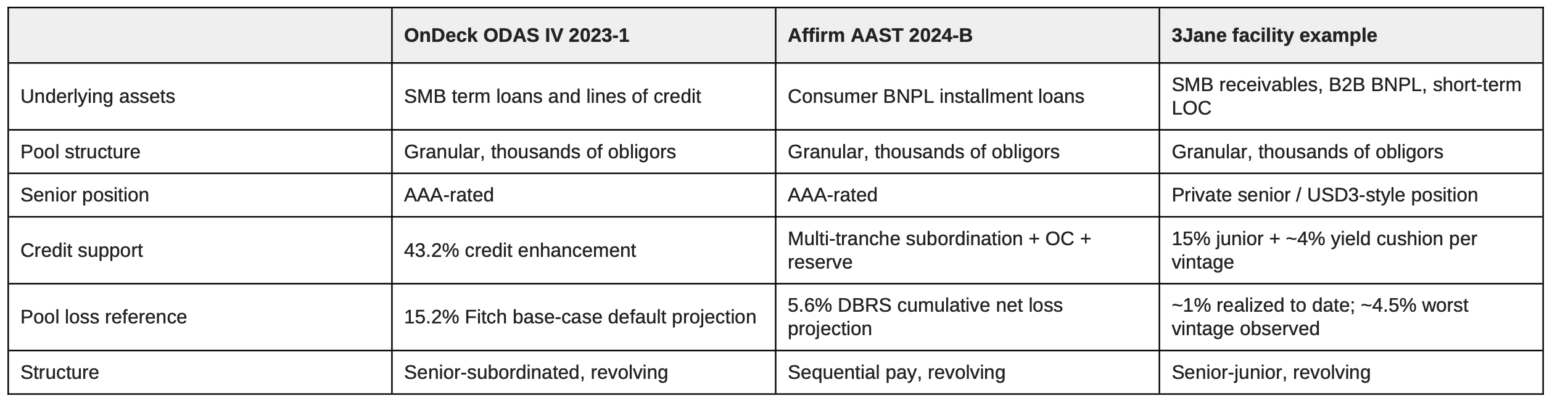

This is how the public ABS market routinely rates granular SMB and consumer receivables pools to investment grade. Two recent transactions illustrate the structural family:

Sources: OnDeck Asset Securitization Trust IV, Series 2023-1 (KBRA pre-sale, July 2023; Fitch base-case default expectation 15.2%); Affirm Asset Securitization Trust 2024-B (DBRS Morningstar pre-sale, September 2024).

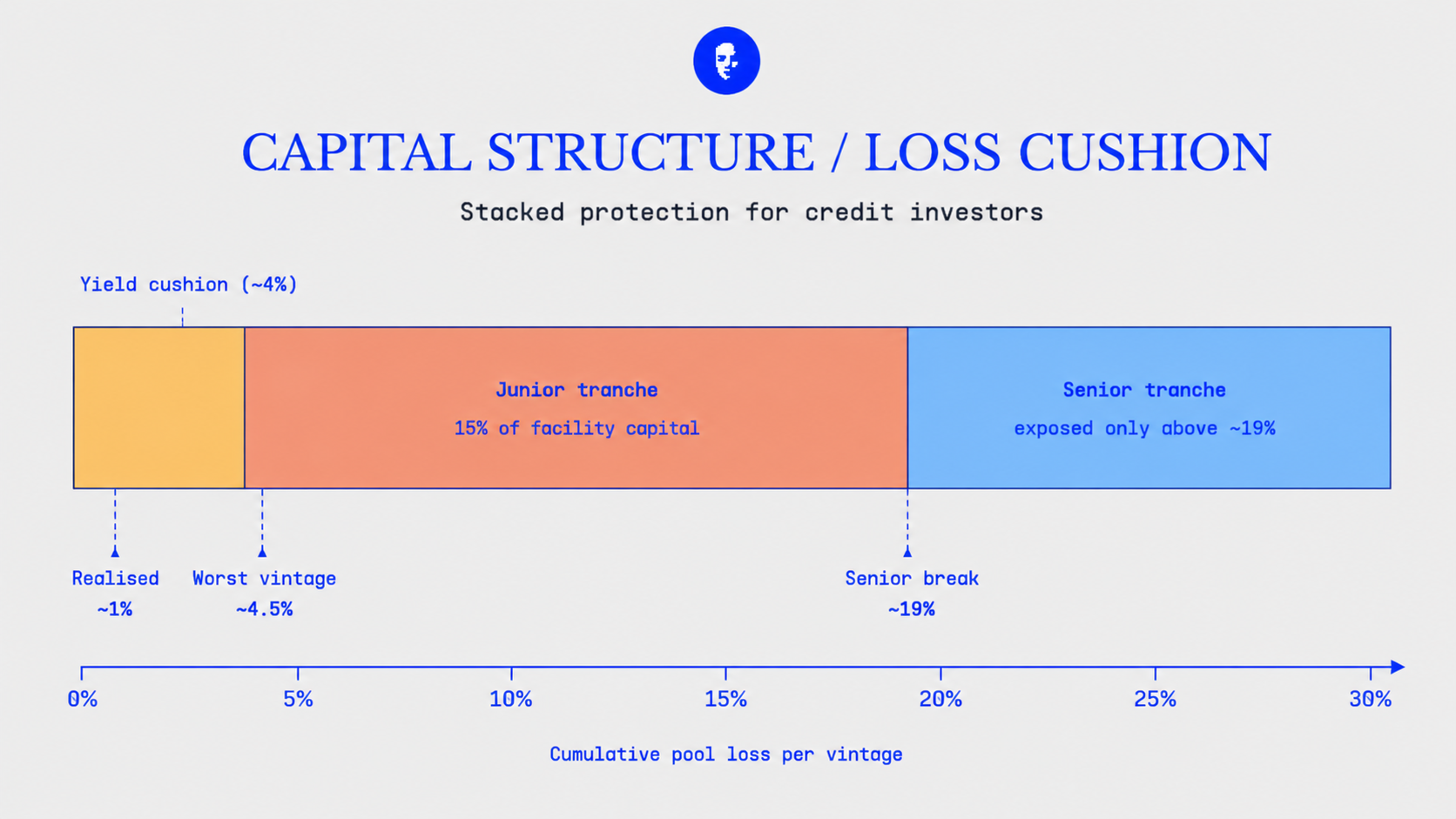

How structuring further compresses the tail

Capital stack on a per-vintage basis. Each cohort of receivables generates net yield over its life that absorbs losses before any principal is impaired; the 15% junior tranche absorbs anything beyond that; the senior tranche takes losses only after both layers are exhausted. Reference markers show realised pool loss, the worst vintage in the book, and the senior break point.

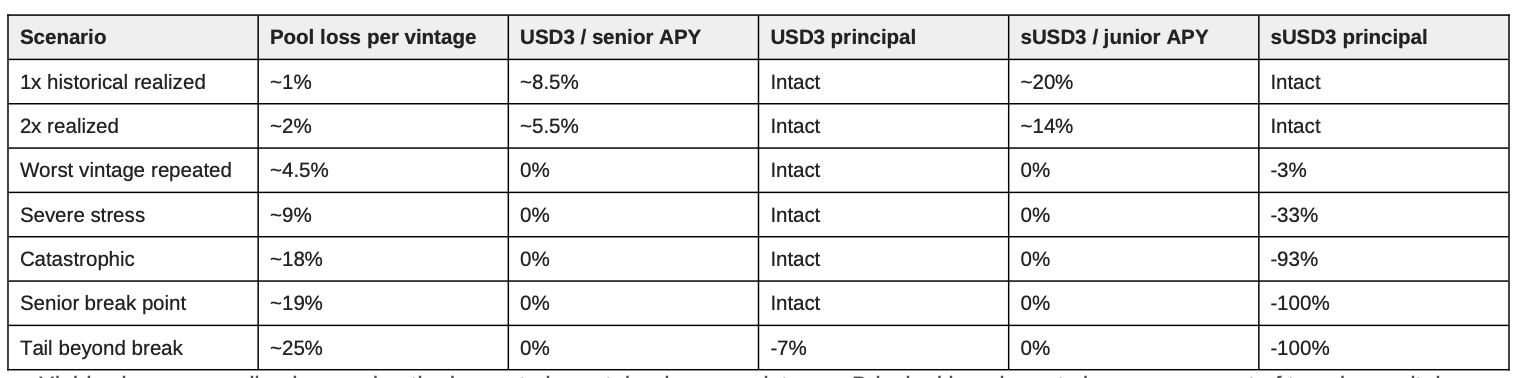

On the receivables book we underwrite, cumulative charge-offs sit around 1% of disbursed principal. The worst single vintage came in around 4.5%, and seasoned vintages collectively run under 2%. The facility example has roughly 4% of yield cushion and a 15% junior tranche, so USD3 / senior first-dollar principal loss starts around 19% cumulative pool loss per vintage.

Borrowers failing together in stress

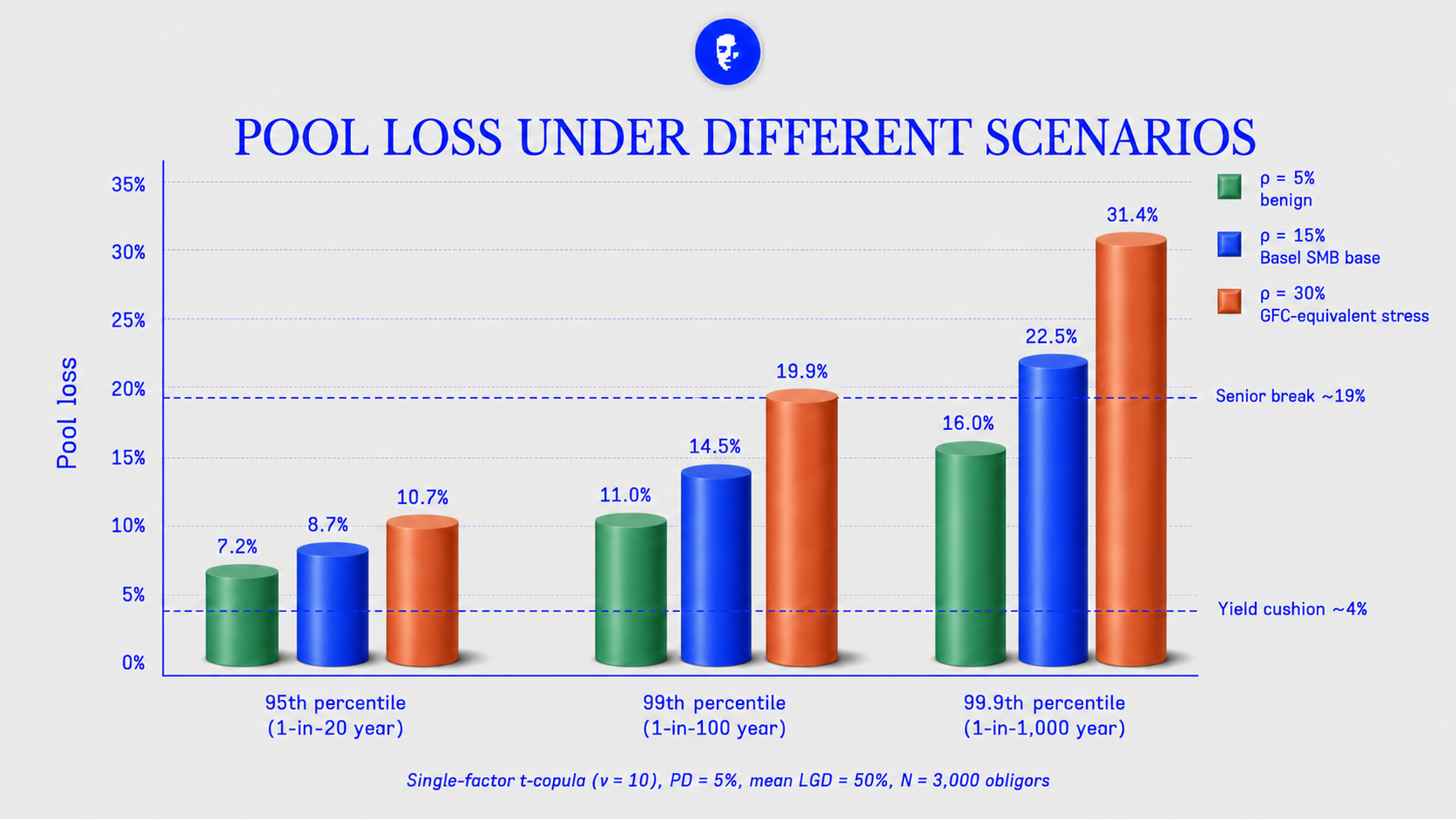

For modelling correlation risk, we pressure-tested the structure using a single-factor t-copula (ν = 10, modestly fatter-tailed than Basel's standard Gaussian framework) at three intra-pool correlation regimes: ρ = 5% (benign), ρ = 15% (Basel's SMB base case), and ρ = 30% (GFC-equivalent correlated stress).

The senior tranche holds up well across the relevant range. At benign or moderate correlation, the 99th-percentile pool loss, an outcome that should occur once a century, sits at 11.0% and 14.5% respectively, well within the junior tranche, leaving the senior position untouched. Even at GFC-equivalent correlation, the gap 99th-percentile pool loss reaches just 19.9%, right at the senior break. The senior tranche only takes meaningful losses in the 1-in-1,000 tail combined with GFC-equivalent correlated stress.

Below is the propagation from pool loss to tranche P&L, scenario by scenario. The senior is untouched until pool losses on a vintage cross 19%. The junior is paid for absorbing everything in between.

The senior receives a high single-digit unleveraged yield for a position whose expected loss is approximately zero and whose tail begins only beyond historically observed SMB stress. The junior tranche absorbs first-loss but is paid a teens IRR with excess spread upside; someone is being paid to absorb base-case risk, and that someone is not the senior holder.